During the past 10 years we have heard competing narratives about the existing degree of synchronization between emerging and developed economies: from talking back in 2008 about the “decoupling” of emerging economies from the US subprime crisis, to defending the “insularity” of the US economy against foreign shocks, particularly those arising from a slowdown in … Continued

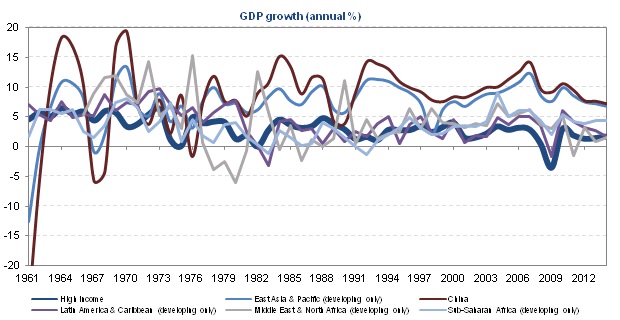

During the past 10 years we have heard competing narratives about the existing degree of synchronization between emerging and developed economies: from talking back in 2008 about the “decoupling” of emerging economies from the US subprime crisis, to defending the “insularity” of the US economy against foreign shocks, particularly those arising from a slowdown in China today. Looking beyond the short-term cycles however, the discussion seems pointless; Globalization has undoubtedly made the world economy increasingly integrated, with the performance of emerging economies increasingly mirroring that of developed ones – with the only exception of Asia – as the graph below illustrates.

In fact, the graph shows an equally important trend: a global deceleration of growth across time; what former Treasury Secretary Larry Summers has termed the “secular stagnation”. Growth in advanced economies has trended down from 5% in 1960 to a mere 1%-2% today. Developing countries have generally not been immune to this illness, with the notable exception of Asia. This singular behavior can be first attributed to the rise of the Asian Tigers in the 70-80s, and later to the conversion of China into a market economy and its incorporation to the WTO. The question now is whether China will be able to decelerate whilst maintaining its “growth buffer” against the rest of the world, or if on the contrary we will witness a sudden dive in growth as that occurred during the Asian crisis back in 1998. At that time Asian economies recovered strongly due to competitive devaluations of their currencies, and in this respect China might be preparing for such a scenario since August’s Renminbi regime change.

The persistent weakness in growth from developed countries coupled with the continuous deterioration of macro data coming from China, has prompted us to position ourselves for an scenario were growth in both developed and emerging markets will further slow down. Consequently, we have massively de-risked our portfolios since August last year by significantly increasing our allocation to US Treasuries and investment grade corporate bonds, and reducing our credit and directional equity exposure.

*Graphic source: World Bank World Development Indicators

Fernando de Frutos, MWM Chief Investment Officer