Post-Pandemic Consumer Disorder BY FERNANDO DE FRUTOS, CFA, PhD | 17 JULY 2022 This article has been published in the FUNDS SOCIETY Magazine (18 Jul 2023) The most anticipated recession in recent history always seems to be 6 months away. High interest rates are cooling down the economy. Yet, consumers are ignoring … Continued

Post-Pandemic Consumer Disorder

BY FERNANDO DE FRUTOS, CFA, PhD | 17 JULY 2022

This article has been published in the FUNDS SOCIETY Magazine (18 Jul 2023)

- The most anticipated recession in recent history always seems to be 6 months away. High interest rates are cooling down the economy. Yet, consumers are ignoring the warnings and refusing to cut back on spending. They have come out of the pandemic wealthier and showing a lower propensity to save.

- With inflation steadily declining and the economy holding up better than expected, the chances of a “Soft Landing” have increased. However, growth is tepid, profit margins are declining, and unemployment could soon start to rise. With the added risk that consumers may tighten more sharply than usual after a period of runaway spending.

- Equity markets have recovered as the economy has dodged the recession. However, they will face increasing resistance. Any sign of market exuberance will encourage the Fed to keep interest rates elevated until inflation is fully under control. This increases the risk of a “Hard Landing”.

Over the past few years, the economy has been on a roller coaster: the pandemic, followed by turbocharged fiscal and monetary policy response, supply chain constraints, rising commodity prices, an unprecedented recovery in the labor market, a massive bout of inflation, and finally, an abrupt cycle of interest rate hikes.

The consensus is that the next turn will be a steep drop. Leading economic indicators (based mostly on surveys) have been blinking red for months. However, the most anticipated recession in history is proving to be elusive; always 6 months away.

In an effort to control inflation, the Fed has markedly increased financing costs. This should cause consumers to spend less and corporations to postpone new investments. This “direct” transmission channel of monetary policy takes time to cool down the economy. Hence the gap we see between gloomy forward-looking expectations and strong data releases.

The manufacturing sector is beginning to prove the forecasts right. These have been pointing to a contraction in activity since November, as the flood of orders created by the pandemic progressively gave way to excess inventories. The service sector, however, is being kept afloat by consumers, who stubbornly refuse to tighten their belts despite all the prevailing pessimism.

Clearly, a “new consumer” has emerged from the pandemic. With a stack of savings, and eager to indulge after the frustration experienced during the lockdowns. A consumption pattern never seen before, characterized by a lower propensity to save and a lessened price sensitivity.

After the initial boom, households reduced spending due to a decline in disposable income in real terms (since salary increases failed to offset inflation). But they are still unwilling to make sacrifices and save preemptively, as would be customary in the face of worsening expectations.

At first glance, this behavior may seem irrational, but it is understandable considering that workers are enjoying a degree of job security never seen before. After all, unemployment is near record lows in most developed economies, and businesses are struggling to find workers.

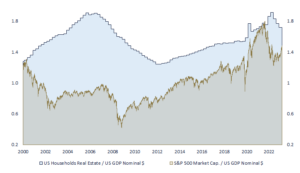

Moreover, the “indirect” transmission channel of monetary policy has only worked halfway, as households (on average) feel wealthier than before the pandemic. Last year we experienced a strong correction in equity markets, but investors have almost recovered their losses. More importantly, despite the rise in mortgage rates, home prices have barely budged.

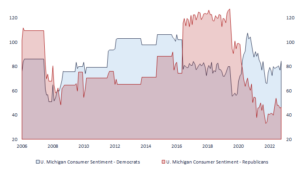

The third element underpinning consumer confidence is the emergence of a “Fiscal Put,” which has replaced the now-absent “Fed Put.” In their minds, citizens (particularly Democrats, looking at the graph below) might be extrapolating from the precedent set by the government’s response to the pandemic; and wonder: if they intervened so forcefully once, why not a second time? Is it really necessary for economies to endure business cycles?

Recessions typically occur when the economy slows down, and consumers preemptively adjust spending in anticipation of a potential rise in unemployment. With a strong labor market, asset prices hovering around all-time highs, and fiscal austerity démodé, it seems we are still a long way from reaching this tipping point.

However, unemployment is a lagging economic indicator. Despite higher labor and financing costs eroding profit margins, companies are “hoarding labor”, afraid to let people go in an environment where workers are still hard to find. But this cannot last forever.

The economy is growing at a low clip and a relatively small drop in consumption can cause it to stall. The biggest risk is that households may tighten more than usual after a period of runaway spending. If this happens, we will discover a new application of Minsky’s famous “stability breeds instability”.

Investors need to be aware of these inherent risks before jumping on the “Soft Landing” bandwagon. Although inflation continues to improve and the economy is doing better than expected, interest rates are going to remain high for longer than expected. Equity markets are going to face increasing resistance to the upside. Any sign of market euphoria may prompt the Fed to continue raising rates, at the risk of breaking the consumer’s back.